In recent posts we have looked at three frameworks intended as guidance for organisations trying to improve their performance. The Balanced Scorecard (BSC) originated as a framework to measure performance, evolved into one for managing performance and finally ended up as one that can also help articulate strategy. Business Performance Management (BPM) came from the ‘other BPM’ (Business Process Management) as a strategic counterpart to the more operational management of processes. Economic Value Added (EVA) originated in the observation that there wasn’t a very robust relationship between conventional measures of financial performance and share price. By rethinking the way profitability is measured, EVA provides a better correlation between financial performance and shareholder expectations.

The purpose of all three frameworks appears similar, but their focus is quite obviously not the same. If we want to improve overall performance in an organisation, how would we go about selecting one of these or, for that matter, any of the wide variety of frameworks from which we can choose?

As we know already, organisations are complex, adaptive, human systems – so each organisation is unique, which means some business performance improvement frameworks might be more suitable for some organisations than for others. Further, since organisations are unique, it is likely that the areas of focus for improving performance are also different for each organisation. One way to identify what an organisation needs is to look for areas of poor alignment, on the premise that improving alignment will improve performance. To do that, we could use an alignment framework such as this one. Using such a framework lets us assess our organisation and put together an alignment profile that shows the areas in which alignment is weak, i.e. an ‘as-is’ alignment profile. We can then consider areas where improvement is most needed, i.e. a ‘to-be’ alignment profile. Based on the gap we can then put together a road map to improve alignment.

But understanding the specific needs of our organisation is only part of the picture. We also need to be able to critically examine alternative frameworks to improve performance so we can select the one that best meets our needs. To do this it is useful to have a big picture in mind, a sort of framework of frameworks, which shows how the improvement frameworks relate to each together. This can help us quickly assess what a particular framework does well and therefore whether it matches what we need. With this goal in mind, let’s take a closer look at EVA and BPM to see how they fit with each other by consider each of the BPM processes in turn to see what role EVA might play.

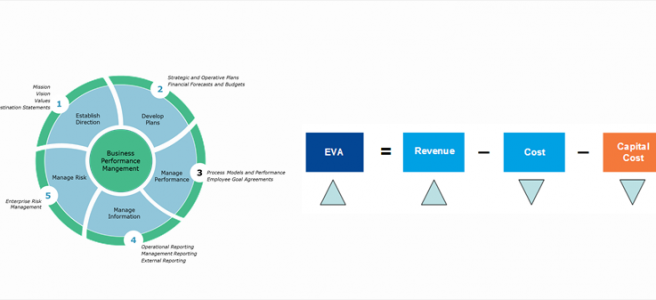

The BPM process Establish Direction results in the articulation of the mission, the vision and strategic objectives (or destination statements). Since the focus of EVA is the investor, the framework is agnostic about the mission of the company, as long as one of the strategic objectives is to deliver the specified level of financial performance.

The BPM process Develop Plans results in the strategic and operative plan, and the corresponding financial forecast and budget. Use of the EVA framework would allow us to assess whether the financial performance we have forecast and the profitability we have budgeted is in line with financial performance targets that match investor expectations. If either falls short, EVA would call for rework of the financial forecast or budget.

The BPM process Manage Performance covers the actions that management needs to take to ensure that business processes operate as required and that employees achieve their goals as agreed. This includes the setting up and adjustment of measures of performance and making interventions to address any gaps between targets and performance. EVA enables improvement in a very specific area relating to this process. By highlighting the cost of capital sitting idle, EVA drives efficiencies in asset management. Otherwise, EVA has a very limited role here.

The BPM process Manage Information delivers a set of performance related data for internal use and external reporting. By specifying adjustments to conventional accounting EVA delivers a picture of financial performance that is better aligned with investor needs for information, but has little to say about any other area of performance reporting.

The BPM process Manage Risk delivers an enterprise view of business risk. EVA focuses on financial risk with a strong emphasis on addressing issues that present risk to investors. One of these risks relates to an acknowledged weakness within EVA, i.e. that an exclusive focus on financial performance can lead to short-termism on the part of executives. The solution is elaborate bonus ‘banks’ that calculate incentives based on performance averaged over three years. This is quite a limited view of business risk and this make strike one as bit odd given the popularity of EVA. The explanation, of course, is that EVA is based on the Agency Theory of organisation. Agency Theory devotes a lot of attention to the risk that the ‘agent’ (the management team) will appropriate more than their legitimate share of profit at the expense of the ‘owner’ (investors).

Now that we’ve looked at how elements of EVA relate to the processes in BPM, let’s reverse our view to look at BPM from the perspective of EVA. EVA clarifies financial performance targets based on market capitalisation and specifies a way in which financial performance is recorded and reported. But when we try to identify EVA processes, it quickly becomes clear that EVA takes a much narrower view of the organisation than BPM.

So is there a way to get the two frameworks to work together? Within the BPM framework, EVA can be seen as a mechanism to align organisational performance with expectations of one particular stakeholder, the investor. A question then naturally follows; do similar frameworks exist for other stakeholders? They do! And next week we will look at one of them.

If you are interested in learning more about organisational alignment, how misalignment can arise and what you can do about it join the community. Along the way, I’ll share some tools and frameworks that might help you improve alignment in your organisation.